Delta Exposure (DEX)

How Directional Positioning Shapes Market Behavior

In the previous post, we talked about gamma exposure and why it explains how the market reacts to price movement.

This one answers a different question.

Before price even starts moving, where is the pressure already leaning?

That’s what delta exposure helps frame.

If gamma tells you how aggressively dealers will need to hedge changes in price, delta tells you where dealers are already positioned right now. One explains reflexivity. The other explains directional weight.

You need both.

What Delta Exposure Actually Represents

Delta is often introduced as a simple sensitivity metric. How much an option’s price changes for a one-point move in the underlying.

That definition is technically correct and practically incomplete.

From a market structure perspective, delta represents directional exposure. When you aggregate delta across all outstanding options, you get a picture of how much directional risk exists in the system.

Delta Exposure, or DEX, is that aggregation viewed through the lens of dealer positioning.

Positive dealer delta means dealers benefit if price goes up.

Negative dealer delta means dealers benefit if price goes down.

Because dealers aim to stay neutral, that exposure matters. It dictates how much directional hedging pressure exists in the futures or underlying market.

DEX is not about curvature or acceleration. It’s about linear pressure.

Dealer Delta vs Trader Delta

Retail traders think about delta as something they hold.

Long calls, short puts, synthetic exposure.

Dealers think about delta as something they must neutralize.

If customers are net long delta, dealers are net short delta. To hedge, dealers buy futures or stock. If customers are net short delta, dealers sell.

DEX attempts to quantify that imbalance.

The exact calculation depends on assumptions. Who owns the options, how hedging is done, which expirations are included. But the purpose stays the same.

It’s not a signal. It’s a structural map of directional risk.

How Dealers Hedge Delta

Delta hedging is mechanical and persistent.

If a dealer is short delta, they need to buy the underlying. If they’re long delta, they need to sell it. Unlike gamma, which becomes more sensitive as price moves, delta hedging is linear.

That matters.

Delta hedging doesn’t explode. It doesn’t suddenly flip behavior because price moved a few points. It applies steady pressure in one direction until the exposure itself changes.

That exposure can change through options being opened or closed.

Price movement alone does not necessarily change total DEX (meaningfully). The market can move without new delta being added. DEX expands when new directional positioning enters or leaves the system.

That’s a critical distinction.

DEX vs GEX

This is where traders often get tripped up.

Gamma exposure tells you whether the market is likely to dampen moves or amplify them. Delta exposure tells you which direction the weight is leaning.

They answer different questions.

GEX: will movement be resisted or reinforced?

DEX: which direction requires hedging pressure?

You can have positive gamma and still trend if delta exposure is heavily skewed. That’s often why markets grind higher in a controlled, low-volatility way.

You can also have negative gamma without follow-through if delta exposure is balanced.

Ignoring one leads to incomplete reads.

Together, they can help explain why some days trend cleanly while others feel unstable and unresponsive.

Practical Implications for Day Traders

One of the most useful ways to apply DEX intraday is by tracking total delta exposure throughout the session.

Think of total DEX as a running measure of how much directional pressure exists in the system.

On trending days, a specific behavior tends to show up.

As price pushes higher, total DEX continues to make new highs or new lows depending on direction. That tells you new directional exposure is being added. Traders are pressing bets and dealers are being forced to hedge in the same direction.

This behavior indicates that we can expect higher prices in the future.

When price continues higher but total DEX stops expanding, that’s information. It means the market is still moving, but new directional exposure is no longer being layered in.

That does not mean an immediate reversal.

It means the trend is losing structural support and is increasingly reliant on momentum alone. Continuation becomes harder.

This is how to think about it:

DEX divergence is not a short signal. It’s a condition change. It tells you to stop assuming effortless continuation and start demanding confirmation from order flow.

DEX is not an entry trigger. It’s a contextual filter.

Used properly, it helps answer a simple question during a trend:

Is the market still being structurally pushed, or is it running on borrowed energy?

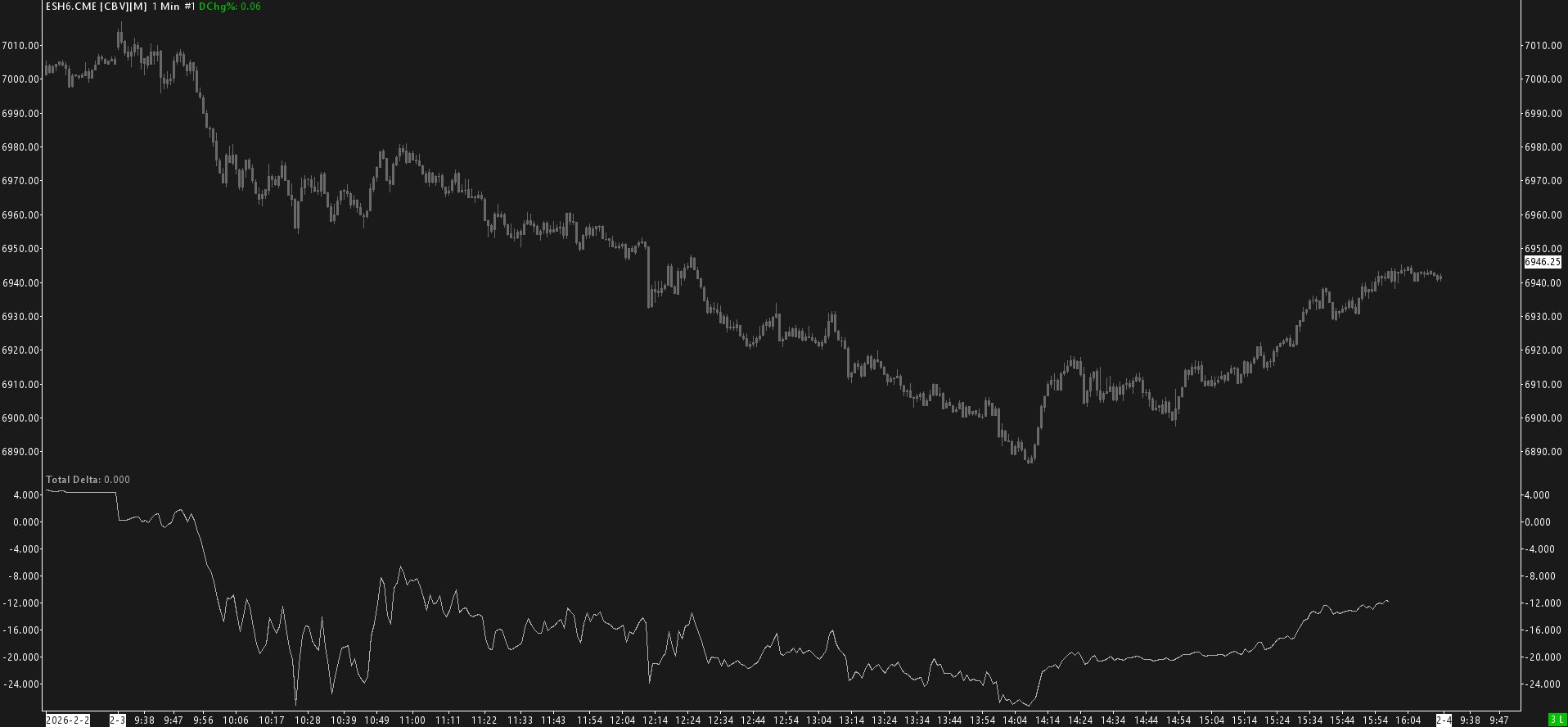

Exercise

Below you’ll find a simple 1 minute chart of the E-mini S&P 500 with a subgraph of Total DEX as it changes throughout the session.

Inspect this chart. What nuances do you notice? What information does it tell you?

Let me know!

Limitations and Context

DEX is a model, not a measurement.

It operates at a structural timeframe. It won’t tell you where to place a stop or when to click buy.

That’s not its job.

DEX works best when combined with order flow, structure, and gamma context. On its own, it’s incomplete. If you integrate it properly, it’s informative and grounding.

Reading the Market’s Starting Position

If gamma exposure explains how the market reacts to movement, delta exposure explains where the weight already is before the move even starts.

That distinction matters more than most traders realize.

Markets don’t move in a vacuum. They move because positioning exists, risk needs to be managed, and hedging flows are forced.

DEX helps you see that starting position.

In future posts, we’ll continue tying these pieces together. Gamma, delta, order flow, and structure. They’re different lenses which help us put together an accurate picture of the market in real-time.

Understanding how they interact is where real edge begins to take shape.

Legal Disclaimer

The content provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, trading, or any other form of advice. All views, opinions, and analyses expressed are those of the author and should not be interpreted as personalized recommendations to buy, sell, or hold any security, futures contract, option, or other financial instrument.

Trading futures, options, and equities involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. You should carefully consider your financial situation, risk tolerance, and objectives before engaging in any trading activity.

The author and Beyond Candlesticks make no representations or warranties regarding the accuracy, completeness, or suitability of the information provided. We shall not be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon.

You alone are responsible for your own trading decisions and outcomes. Consult a qualified financial professional before making any investment or trading decisions.